MacroScope

One day following the Fed’s 50bps hike, the BoE and ECB followed suit with similar hikes that had been widely expected, but the lack of conviction to tightening by the BoE contrasted sharply with the decisiveness of ECB. The day was packed with mixed economic data while markets reacted to the collective tightening with steep declines in equities and fixed income, and a rebound for the dollar.

Cracks in China from Covid restrictions

China’s update of economic activity during November reflected the impact of harsh restrictions that were still in place at the time, and a real estate market that will take years to stabilise. Retail sales were 5.9% lower than last November against a forecast decline of 4%, industrial production climbed 2.2% but missed the 3.5% increase expected, and property investment accelerated its decline to 9.8%. With restrictions now being relaxed, activity should start to recover, subject to the challenges from surging Covid deaths and infection rates.

BoE promises to get tough on inflation

The Bank of England’s 50bps hike to 3.5% came as no surprise with markets only unsure of the extent of MPC division. Six members voted for the 50bps hike, while Catherine Mann saw “greater evidence" that price pressures "would stay stronger for longer" and voted for a 75bps hike. The always dovish Swati Dhingra - who believes rates were already restrictive at 2.25% while inflation rates at double digits - was joined by fellow dove Silvana Tenreyro in voting to leave rates unchanged.

Bank staff revised their November forecast of a .3% contraction in GDP this quarter to a much milder contraction of just .1%, but the statement noted the economy was still “expected to be in recession for a prolonged period”. However- perhaps reflecting the conflicts of opinion on the Committee, - if the economy evolves as the Bank expects, the majority of the MPC judged that “further increases in Bank Rate may be required for a sustainable return of inflation to target”. The labour market was described as “tight” with the ratio of vacancies to unemployed at “a very elevated level”, and although CPI inflation is still expected to remain “very high in the near term”, the Bank expects it but to plunge below the 2% target in two years’ time.

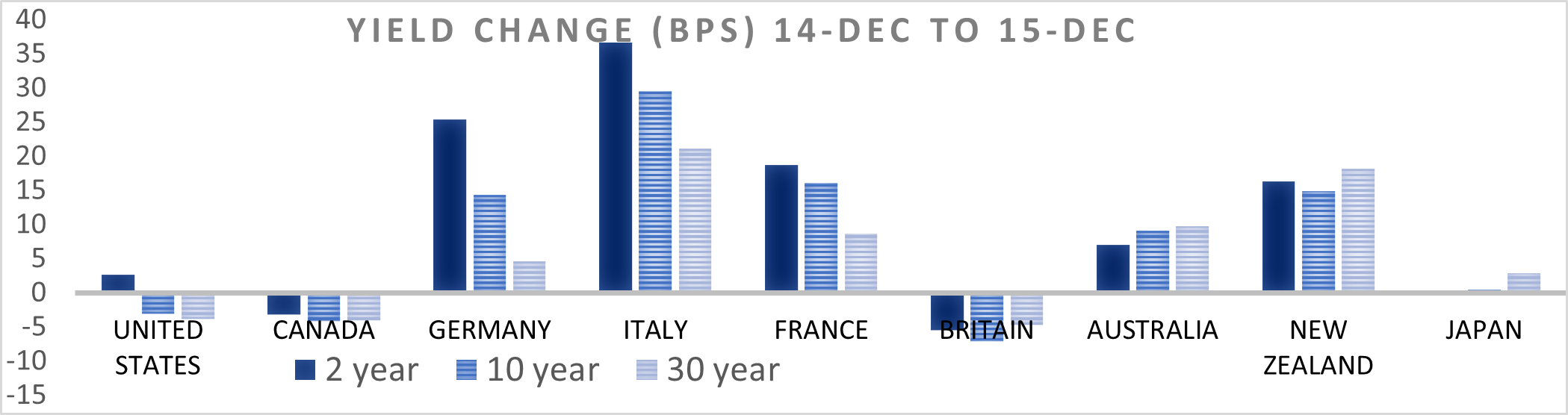

Market reaction to the deep divisions in MPC members’ opinions and a statement that seemed short of credibility reflected doubts over the Bank’s commitment to “respond forcefully” if it sees “more persistent inflationary pressures”, with sterling sinking 2.1% to $1.2159 and the two-year gilt yield declining to 3.4% (-5.5bps).

Lagarde brings a gun to the inflation knife-fight

The ECB’s 50bps hike was accompanied by a decisively hawkish statement, the announcement of the start of quantitative tightening, and hawkish press conference that left markets in no doubt of the direction of travel. Lagarde said “We have more ground to cover, we have longer to go and we are in for a long game” as she warned the ECB expects “to raise interest rates at a 50 basis-point pace for a period of time” and that markets are under-pricing the amount of further tightening needed.

The ECB updated its economic forecasts, with inflation expected to stay high - despite declining to 10% in November from October’s record high of 10.6% - and to not reach the 2% target even after three years. Growth this year is expected to be higher than forecast in September, but next year’s estimate was cut from .9% to .5%.

Quantitative tightening will begin in March and involve partially halting the reinvestment of maturing bonds purchased under the Asset Purchase Program, with a pace that will average €15 billion a month in the second quarter.

The market reaction following the ECB meeting was in stark contrast to the BoE, with the yield on the 2-year bund jumping 25bps to 2.39% and the euro/sterling cross-rate closing over 1.6% higher in London at £.8717. Italy’s BTP’s were hit hard, with an increased fiscal deficit in the budget likely to be passed by the new Meloni government before the end of this year leading to greater supply, while private purchasers will also need to fund the reduced demand from the APP, as the two-year BTP yield jumped 37bps to 3.01% and the ten-year closed at 4.15% (+30bps).

Earlier in the day, there were encouraging signs of less pessimism over the Eurozone outlook. Germany’s IfW economic institute revised its outlook for 2023 GDP from a contraction of .7% to a .3% expansion, with inflation now forecast to be 5.4% rather than 8.7%. The French INSEE Business Confidence survey for December was unchanged from November at 102 but importantly, it remains above its long-term average of 100.

Little Christmas cheer for US retailers

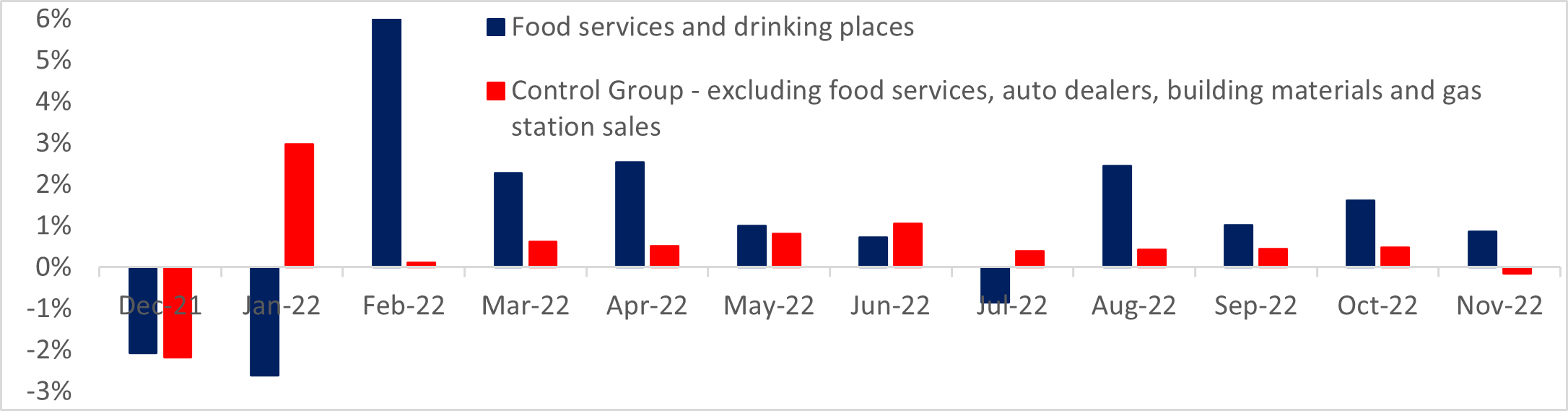

US data were mixed but disappointing on balance. Retail sales sank more than expected in November, with a .6% month on month decline unwinding some of October’s 1.3% increase. Spending on motor vehicles, furniture and building materials were each roughly 2.5% lower although the figures are in nominal terms and may partly reflect lower prices in those categories. Sales in the Control Group – which feeds the GDP calculation - were just .2% lower but missed estimates for a .1% increase, with a two tenths downward revision to the prior month compounding the disappointment.

Retail sales represent only 40% of US consumption with services comprising 60%, and the only glimpse of services consumption in the retail report is from spending at bars and restaurants which rose .9% on the month. According to Oxford Economics, consumer spending remains healthy in the fourth quarter, and “even with the decline, control retail sales were up 4.6% annualized over the prior three months”.

Claims show little loosening of the labour market

Initial claims declined 20K last week to 211K while continuing claims from the prior week were virtually unchanged at 1.671m. It is too early to know if the recent upward drift in claims is being reversed, particularly with typical noise in the data around the Thanksgiving holiday, but the low levels anyway suggest employers are still clinging tightly to workers with widely acknowledged difficulty in replacing any that leave.

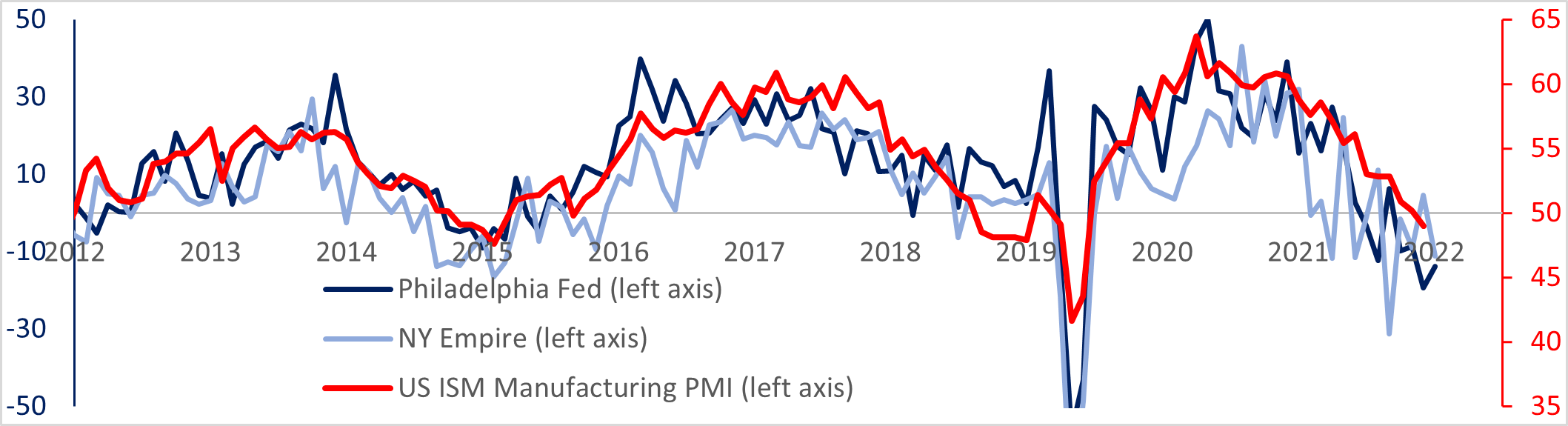

US surveys and hard data signal weaker manufacturing sector

The Empire and Philly Fed manufacturing surveys moved in opposite directions once again in December, although both were weaker than expected and both signalled contracting levels of activity. The headline General Business Conditions index of the Empire sank 15.7 points to -11.2 while the Philly Fed General Activity index rose 5.6 points but remained negative at -13.8. The one uniformly positive aspect of the reports was an improvement in the outlook, with the Empire index for future business conditions improving 12.4 points to 6.3 and the Philly Fed future general activity index rising 10 points to 3.8 – its first positive reading since May.

Industrial production declined .2% in November but an upward revision of September’s .1% increase to .4% offset some of the disappointment to estimates of an unchanged reading. Manufacturing production fell .6%, weighed down by a 2.8% plunge in the output of motor vehicles and parts.

Markets

Tighter central bank policies took their toll on many markets, with Wall Street having a delayed reaction to the prior day’s FOMC meeting.

Fixed income

European yields closed sharply higher with the bund curve inverting further. Ahead of the European open, Antipodean yields had also closed higher after Australia reported employment growth of 64K in November – more than three times the 19K expected with an 11K upward revision to the prior month, while New Zealand’s third quarter growth of 2% (quarter on quarter) was more than double the .9% expected.

Commodities

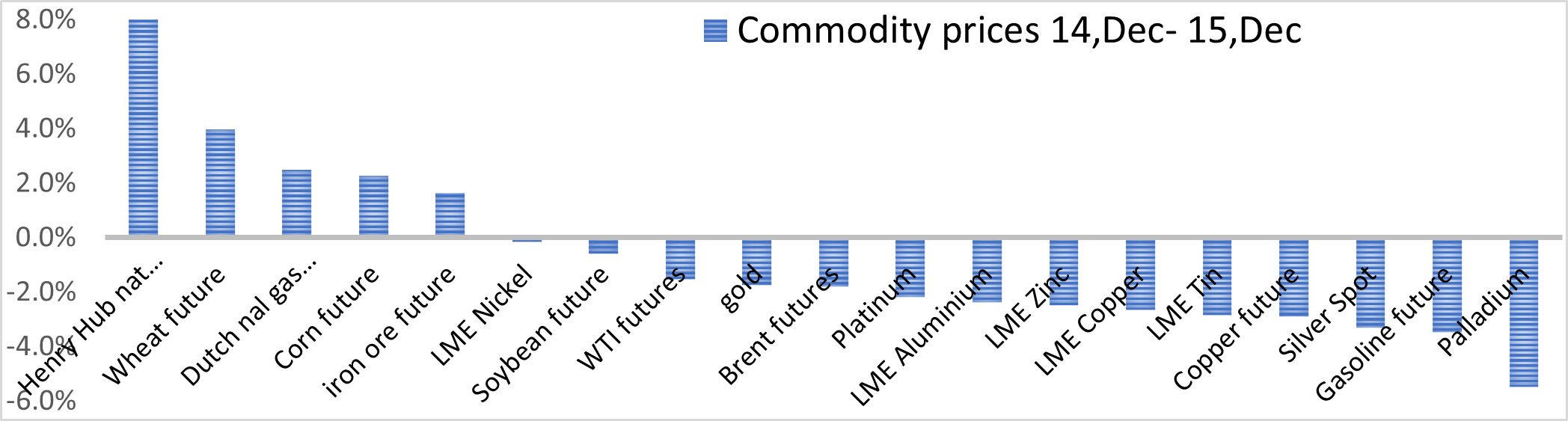

Precious metals were flattened following the tighter Fed policy but reaction elsewhere in the commodity complex was limited.

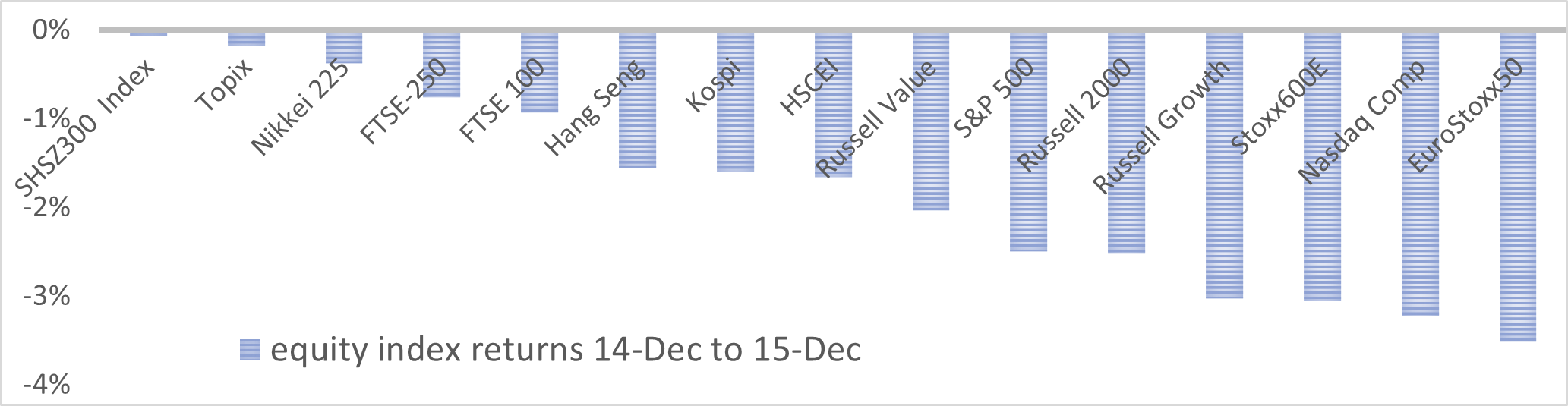

Equities

No major equity index escaped unscathed, while European equities were hit particularly hard.

Today’s events

Japan Jibun Bank composite PMI December

UK GfK consumer confidence December, retail sales December

S&P December PMIs for the Eurozone, France, Germany, the US and the UK December