MacroScope

Hopes for an earlier end to the hiking cycle were boosted by a speech from Powel last week, and despite mixed signals on the strength of the economy, the promise of a pared-back rate hike and renewed interest in fixed income investments pushed the dollar to an almost 6-month low and added support to the equity rally that began in October. Friday’s payroll report should have dampened investors’ enthusiasm, with pay growth that was propelled by continued strength in labour demand, but renewed risk appetite and forced short covering have given markets upward momentum that currently seems unstoppable.

Positive data surprises earlier in the week had little impact on the bond market rally, with investors focussed purely on anything that might bring forward the start of easier policy. A dip below 50 in the ISM manufacturing index satisfied the collective confirmation bias while evidence of renewed economic strength was dismissed. Third quarter growth was revised three tenths higher to 2.9% and consumption looks to have started the fourth quarter on the front foot, with real consumer spending growth of .5% in October – the most in 15 months – closely matched by real personal income growth of .4%. However, surveys are pointing to a slowdown in activity and recession warnings are growing increasingly loud. According to the Philadelphia Fed survey of professional economists, there has never been a higher share of respondents expecting a recession over the next twelve months since the survey began in 1969.

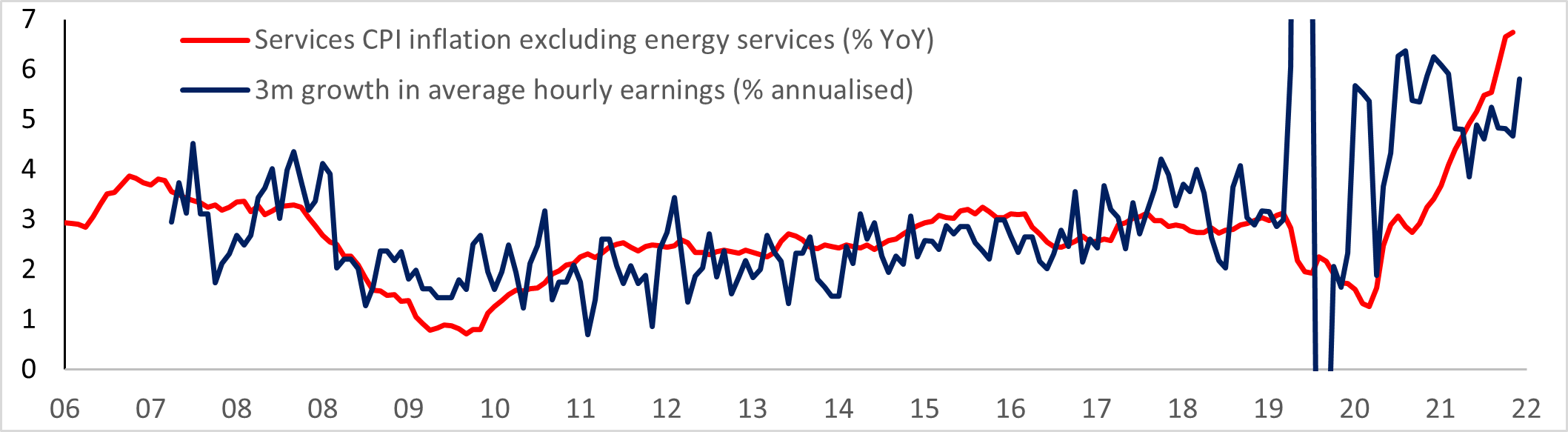

Job growth of 263K in November compared with 200K estimated, and the acceleration in average hourly earnings growth to .6% on the month was double that expected, matching the strongest monthly increase since December 2020. Year over year average hourly earnings growth accelerated to 5.1% and the annualised rate of growth in the three months to November was 5.8% - a much faster rate than the 3.9% that was originally reported in the three months to October (prior to Friday’s upward revisions to the data). Powell’s speech had stressed the importance of a moderation in wage growth, and a rapid acceleration like this is unlikely to sooth concerns over persistent service sector inflation.

In Europe - where fears of an energy crisis are weighing heavily on sentiment – the most important economic releases last week gave little reason for the ECB to signal an end to the hiking cycle. Unemployment across the region fell to a record low of 6.5% in October while core inflation of 5% remained at a record high, but the doves on the Governing Council probably have enough survey evidence of slowing activity to limit next week’s hike to 50bps.

Consumer confidence and industrial PMIs have been signalling a slowdown for some time – the S&P manufacturing PMI for the Eurozone first dipped below 50 in July although industrial production across the region was still growing in September. Friday brought the first of the October figures and the signs were not good - French manufacturing production sank 2% on the month and was unchanged year over year, with overall industrial production dropping 2.7% year over year. Separate data from last week also hinted at a less healthy consumer sector at the start of the fourth quarter, with French consumption and German retail sales both dropping 2.8% in real terms during October.

Economic data from China comprised mainly purchasing managers indices which signalled a faster slide into contraction. Hopes of renewed stimulus and a slight relaxation of Covid restrictions drove the HSCEI over 29% higher during November – the best monthly return since Dec 2003 – and as the economic suicide and public rejection of current policies become increasingly apparent, progress towards looser restrictions will hopefully continue.

Markets

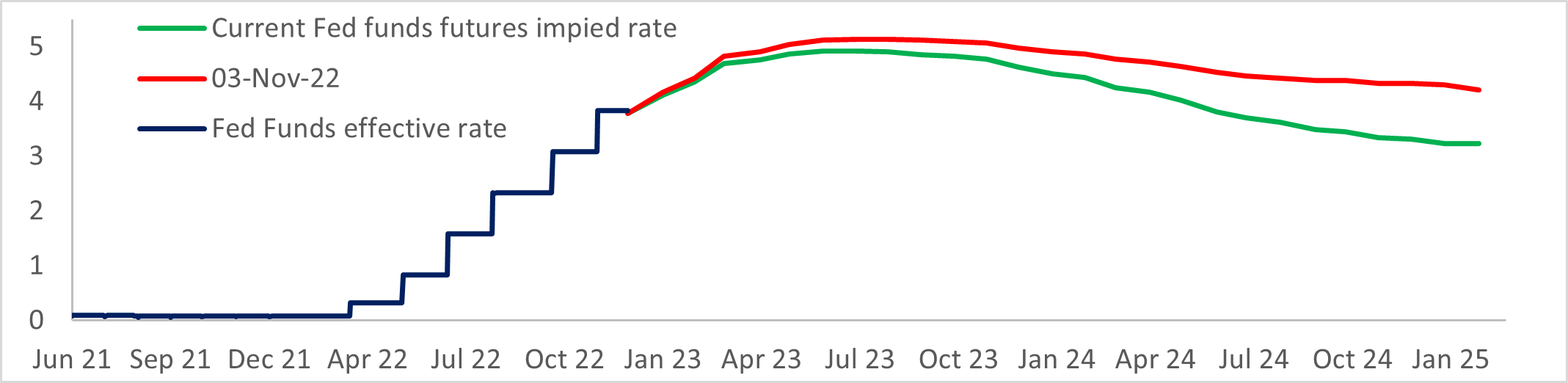

The ten-year treasury yield spiked 13bps after Friday’s payroll release but closed the day 2bps lower at 3.49%, while the two year yield which had earlier taken back some of the rate cuts priced to start next summer, ended the day just 4bps higher. Money markets are pricing a peak in the Fed funds rate that is roughly 25bps lower than was expected a month ago, and a rate at the end of 2024 that is more than a percentage point lower.

Former IMF head Olivier Blanchard wrote in the FT that as the economy slows next year and inflation declines, the Fed’s inflation debate will centre on “whether it is worth getting it down to 2 per cent if it comes at the cost of a further substantial slowdown in activity”. Without formally changing the 2% target, the Fed may well accept an inflation rate of 4% to avoid the labour market damage from overly aggressive tightening, with the added benefits of maintaining growth and deleveraging of the economy faster. History has shown that the Fed’s inflation fighting resolve tends to buckle in the face of higher unemployment, and regardless of Powell’s pledge to avoid the mistakes of the 1970s, markets are convinced that the tightening cycle will soon be reversed.

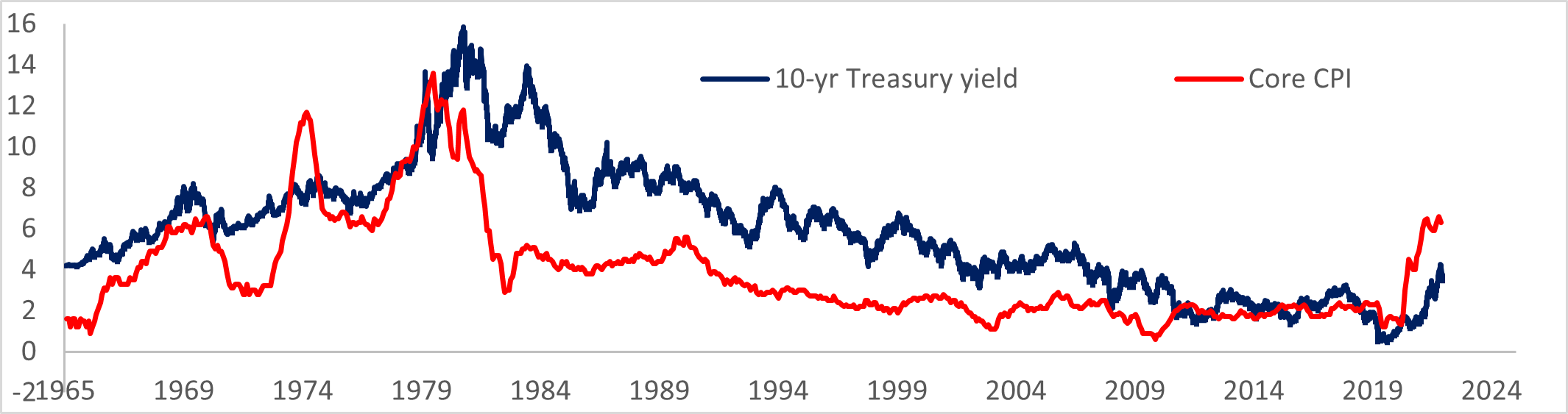

This leaves longer end yields vulnerable to inflation that may again prove itself to be more persistent than officials expect, with a ten-year treasury yield that eventually crosses back above the rate of core CPI inflation.

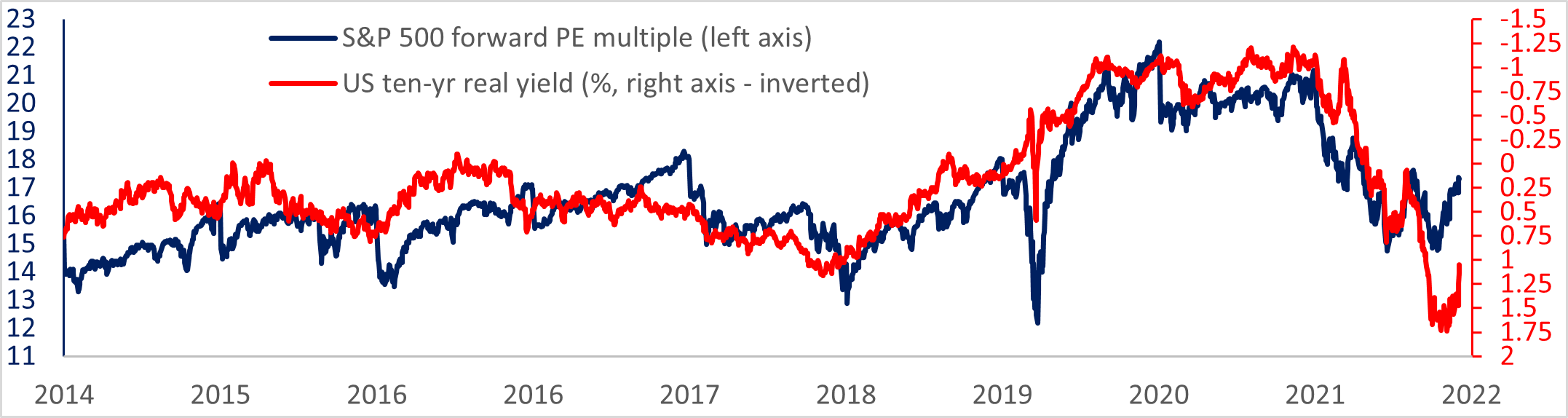

That risk is not currently a concern for markets, which see the Fed softening its stance on inflation in preparation for an economic slowdown that may not match the dire forecasts from analysts. The real rate on ten-year treasury TIPS accelerated its plunge from 1.74% a month ago to 1.05% at Friday’s close, weakening the dollar and giving a boost to all asset classes from precious metals and crypto currencies to equities and credit.

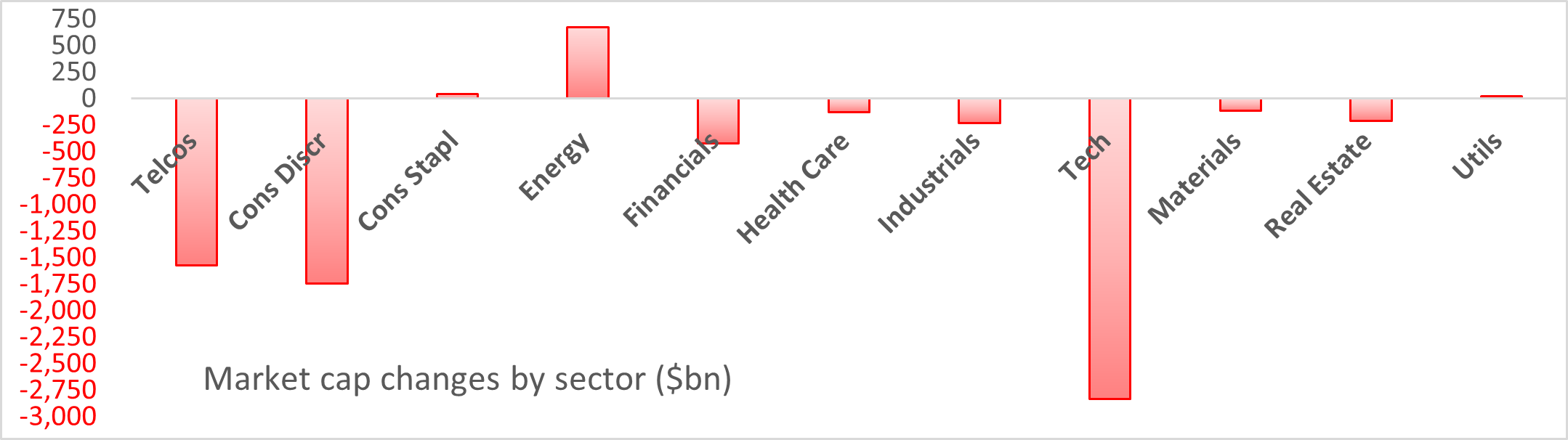

At Friday’s close the S&P 500 had recovered well from its worst levels, for a year-to-date loss of 15.5%. Tech has been responsible for 43% of the $6.5 trillion of market cap destruction in the index, thanks to sky high valuations at the start of the year that could not be supported by growth prospects, while Energy was one of the few sectors providing an offsetting increase in market cap over the year.

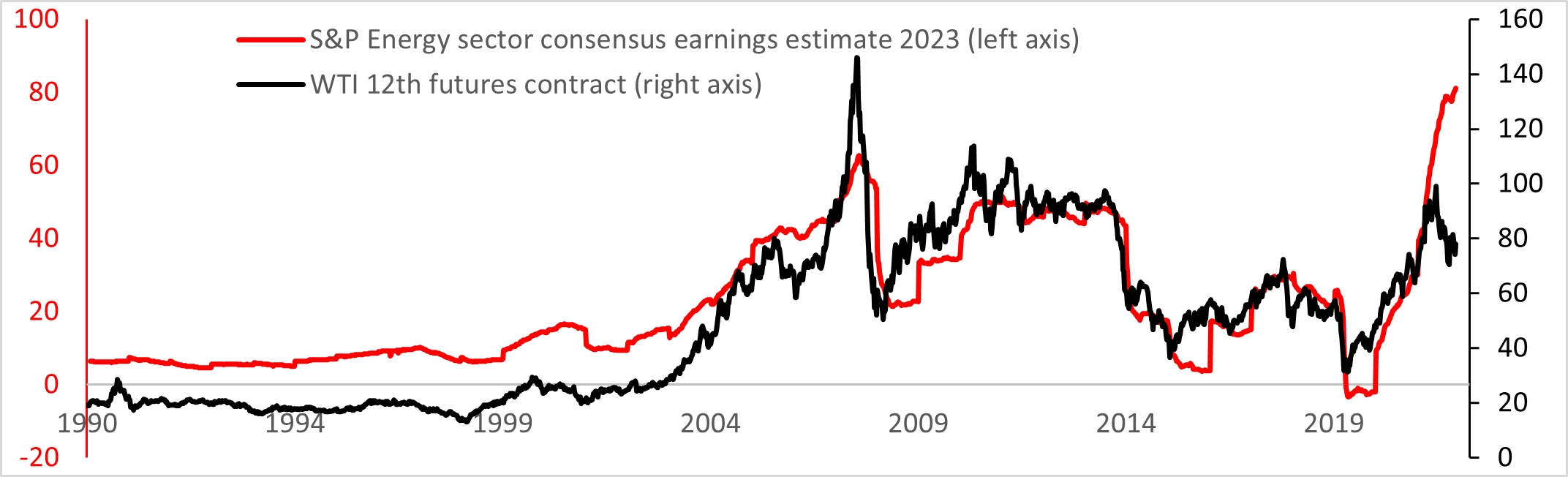

Energy sector earnings estimates now look to be living on borrowed time. Crude prices are vulnerable to signs of an economic slowdown and have been on a steady decline since June, but earnings forecasts from the sector have so far shown no response.

The relative performance of the major S&P groups will undoubtedly have a different pattern next year, but for the overall index, a multiple of around 17 based on estimates of next year’s earnings is not too challenging. The important issue is whether those estimates will hold up in the face of stiff economic headwinds.

The economic agenda for next week is relatively light, and further position squaring should be expected ahead of the following week’s final CPI print of the year and the final FOMC meeting.

Monday 5th Dec

Italy and Spain S&P services PMI November, EU retail sales December, Sentix investor confidence December

UK new car registrations November

US ISM services index November, factory orders October

Tuesday 6th December

UK BRC like-for-like sales November

Germany factory orders October

US trade balance October

Wednesday 7th December

Germany industrial production October, Italy retail sales October,

US weekly MBA mortgage applications

Thursday 8th December

UK RICS house price balance

US weekly initial and continuing clams

Friday 9th December

US PPI inflation